Leading global real estate advisory and property agent Savills has released its latest Branded Residences Report for the Americas. This comprehensive analysis covers the branded residential sector across North America, the Caribbean and Latin America

The report highlights the region’s continued dominance in the global market, with 370 completed schemes representing 45 percent of the worldwide total and a robust pipeline of over 350 projects expected by 2032.

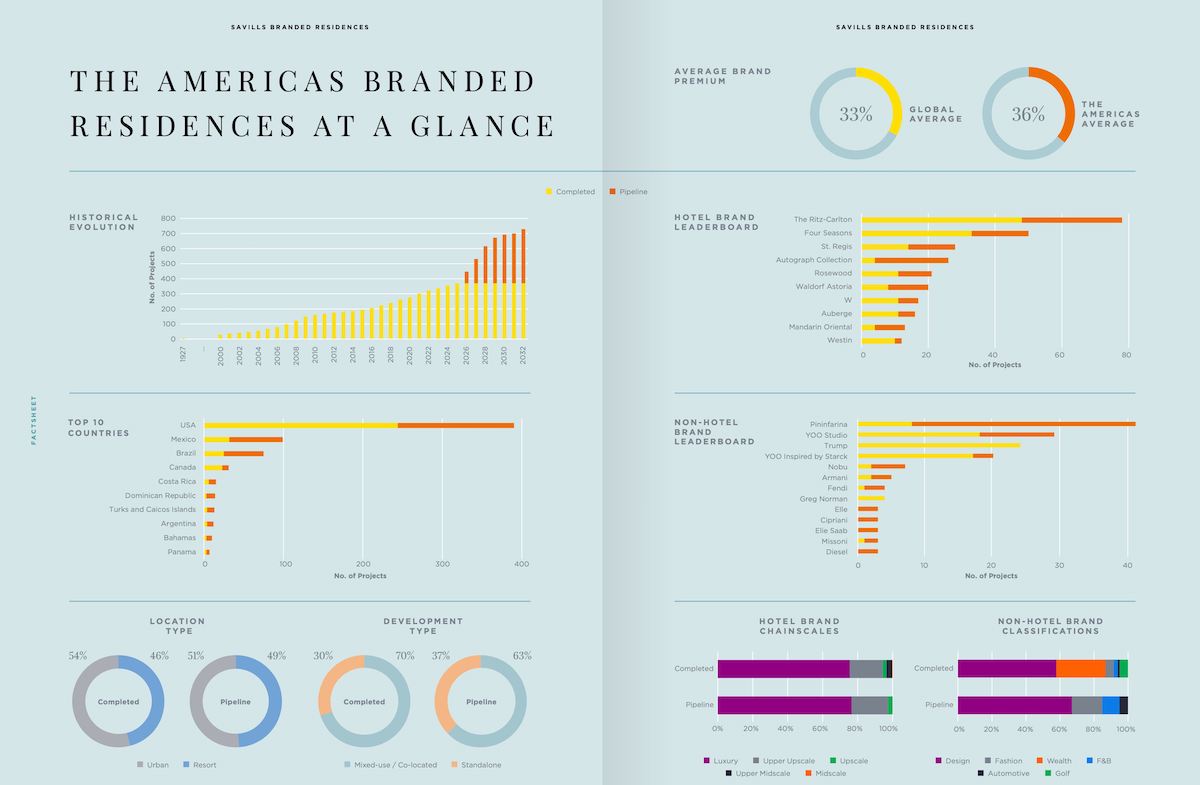

Other key findings include an increased 36 percent average brand premium (current global average 33%), significant growth in Caribbean and Latin America (CALA) markets, continued leadership from Marriott International , and the rising influence of non-hotel brands such as Pininfarina.

The Americas Branded Residences at a Glance

Branded residences in the Americas have shown steady historical growth since the first project, the Sherry Netherland in New York in 1927. Today, the region maintains a balanced mix of urban and resort locations, with completed projects split roughly evenly.

Pipeline projects indicate continued momentum, particularly in standalone developments, which are expected to rise from 30 percent of completed schemes to 37 percent by 2032.

Top countries by number of projects (completed and pipeline) include the USA (leading by a wide margin), followed by Mexico, Brazil, Canada, and Costa Rica.

Development shows a near-even split between urban and resort, and while mixed-use or co-located projects still dominate the sector, standalone schemes are gaining ground.

Growth and Geographical Breakdown

North America remains the dominant force globally for branded real estate development. It benefits from its maturity and established markets.

The USA leads with over 140 projects in the pipeline, although growth is moderating in many areas as the market matures. Florida particularly Miami stands out as a major exception, with an expected pipeline growth of 127 percent. This growth is driven by the year-round lifestyle appeal, a strong luxury real estate market and favorable tax conditions.

CALA represents the region’s most dynamic growth story. Currently accounting for 28 percent of completed schemes in the Americas, this share is projected to surge by 194 percent by 2032.

Key drivers include rising domestic purchasing power in gateway cities like Mexico City and Sao Paulo, along with international demand for resort destinations such as Riviera Maya, Los Cabos, and Punta Cana.

Although the Americas are expected to see their global share of branded schemes decline slightly to 39 percent by 2032 as other regions, particularly the Middle East and Africa, accelerate, the absolute numbers remain impressive and reflect sustained confidence.

Structural Trends

The report notes a balanced urban-resort split across the Americas, but with clear regional differences. North America favors urban projects (60 percent), particularly in high-demand cities, while CALA leans heavily toward resort locations (60 percent). In these areas, branding helps build buyer confidence in less mature luxury markets.

Standalone developments are becoming more prominent not only in the Americas but globally. This shift is driven by both the growth of non-hotel brands and hotel brands’ willingness to operate without co-located hotels.

The change allows brands to monetise equity with lower operational complexity in markets where residential demand outpaces hotel needs.

Brand Premium

The Americas deliver a 36 percent average brand premium, up from 32 percent the previous year and above the stable global average of 33 percent. Premiums remain strong across both resort and urban projects.

While North America’s mature markets show tighter premiums, CALA’s emerging status supports higher uplifts.

Core fundamentals of (prime location, appropriate brand selection, and proper scale) continues to unlock meaningful premiums even in established markets like the United States.

The Leading Brands

Marriott International maintains a commanding lead with more than three times as many projects as its nearest rival. It is supported by a pipeline exceeding 100 projects, particularly through The Ritz-Carlton and Autograph Collection.

The Autograph Collection brand is demonstrating exceptional growth, and is forecast to grow from just four projects currently to 26 projects by 2032.

Other active hotel groups include Accor and Hyatt, both with pipelines surpassing their current stock. Mandarin Oriental are also showing strong growth, being the only other hotel brand in the Top 10 where their pipeline is more than double the number of their completed schemes.

On the non-hotel side, Pininfarina leads with the largest overall pipeline of 35 projects. This places it third on the combined leaderboard.

Design brands in general continue to dominate, but Fashion, F&B, and Automotive sectors are becoming increasingly popular with property developers wanting to develop something new and fresh (less hospitality-focused) to appeal to a different buyer profile who favours design aesthetics and brand loyalty rather than a purely hospitality-focused lifestyle.

Consumer brands are entering the market at pace with the most recent being the premier lifestyle, entertainment and investment company Palm Tree Crew with Palm Tree Residences in Miami.

Our data shows that there are almost 100 non-hotel brands active in the sector from more than 20 different industries.

Regional Outlook

The Americas are expected to enjoy a 97 percent growth rate through 2032. This matches other mature regions but demonstrates structural rather than cyclical demand. This resilience stems from high-net-worth individual growth, increased global mobility, and a service-oriented culture.

North America provides scale, stability, and product diversification, while CALA serves as the primary growth engine. CALA growth is driven by tourism, international funding, and demand for resort-led properties. The United States remains the global benchmark for innovation in branded residential structures and pathways.

The report concludes that the Americas branded residences sector is maturing thoughtfully. Strong fundamentals support continued expansion across its dual-track trajectory of established and emerging markets.

Download and read the full Savills Branded Residences Report The Americas